From Myth to Reality: The Scalable Stablecoin

·

6

MINUTES

·

By:

Ari Pingle

Yield in crypto is compressing.

sUSDe is at 3.3%. Aave is at 3.4%. Treasury-backed stablecoins are capped at the risk-free rate, currently 3.7% and potentially set to fall when Warsh gets sworn in. Across the board, crypto yield is approaching the same ceiling: the risk-free rate.

This is not a moment in time. Instead, it’s structural.

That compression reveals the real issue: crypto cannot scale yield (at least in the short-medium term) by recycling capital onchain.

Onchain yield has been powerful, but it is ultimately constrained by the size, leverage, and risk appetite of the crypto market itself. To build yield products that can scale to billions, tens of billions, and eventually far beyond that, crypto has to access yield from markets much larger than itself.

That means traditional finance.

TradFi is not just a larger market. It is the global market. It includes commodities, credit, trade finance, treasuries, derivatives, inventory financing, receivables, and the real economic flows that power the entire world. These markets have far greater capacity than crypto-native markets because they are tied to actual global demand, production, consumption, and financing needs.

RWAs are the bridge. They allow crypto users to access real, massive traditional markets through crypto rails. They bring offchain yield onchain in a form that is transparent, composable, and globally accessible.

We built thUSD around that idea. The thesis is simple: a stablecoin’s yield can only scale if it sources yield from markets larger than crypto itself, holds up when crypto doesn’t, and routes through architecture institutions can underwrite.

Our three structural requirements were scale, durability, and security.

Here’s how thUSD does each.

1. Scale

Crypto-native yield is limited because it can only come from other onchain participants. Since the pool of borrowers, traders, and speculators is finite, competition for that yield increases and returns tend to shrink over time.

thUSD breaks out of that constraint by sourcing yield from traditional markets with far greater depth and capacity.

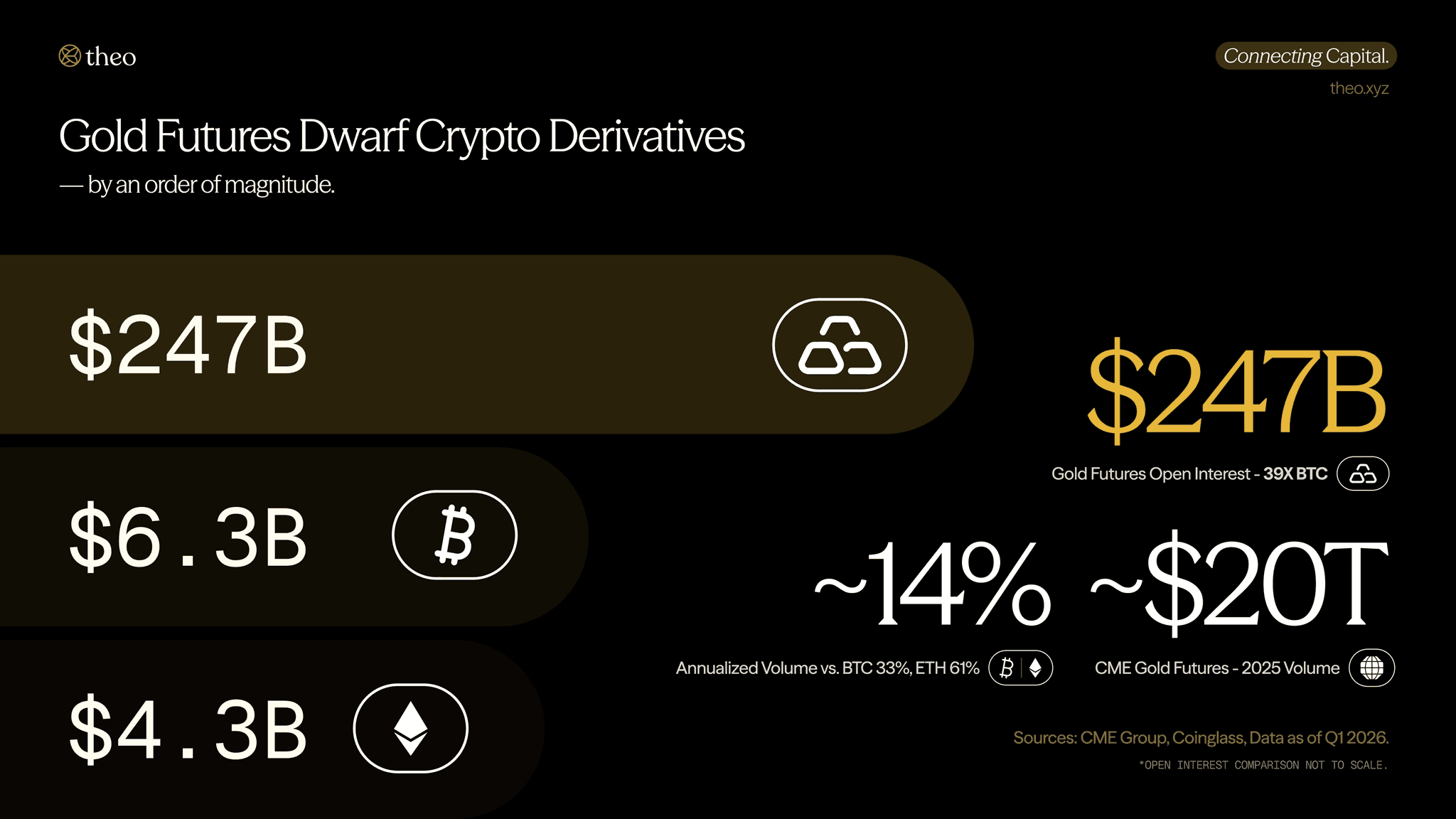

Its core yield comes from CME gold futures, a market with more than $250B in open interest that traded almost $20T in 2025. Annualized volatility is roughly 14%, less than half of BTC and a quarter of ETH. It is one of the deepest and most liquid commodity derivatives markets in the world.

More importantly, the yield comes from market structure. Spot gold consistently trades below futures. That basis exists because commodity markets need to clear. Producers hedge forward production, consumers lock in future delivery, and carry sits between the two. The result is a structural yield source tied to global commodity markets rather than onchain lending demand.

This is the core promise of RWAs: crypto users can access yield from real traditional markets without needing to leave crypto rails. The opportunity is not to manufacture more yield inside crypto, but rather to connect crypto rails to the massive pools of yield that already exist across the global economy.

2. Durability

Scale is necessary, but it means nothing if the yield disappears when market conditions shift.

Crypto-native yields tend to rise when risk appetite is high and vanish when conditions tighten. Lending rates fall when leverage leaves. Funding rates compress when traders reduce exposure. Treasury-backed products remain capped by central bank policy. That makes most onchain yield highly dependent on crypto cycles.

thUSD is built around a different kind of yield: yield that comes from real-world market structure. In March, Strait of Hormuz tensions drove one of gold’s sharpest monthly declines since 2013. The same event crushed crypto funding rates, pushed oil near 2022 highs, and complicated any near-term path to rate cuts.

Every other yield source got squeezed from both sides, but gold carry held. This is the difference between yield that depends on leverage and yield that depends on real market function. One is cyclical. The other is structural.

That distinction matters because the future of stablecoin yield will not be won by products that chase the highest temporary APY. It will be won by products that can absorb serious capital and continue paying through different market environments.

3. Security

Two weeks ago, I wrote an article titled DeFi isn’t dying, it’s dividing. The short of it was that speculators will remain onchain-native, while savers will move toward RWAs that offer crypto rails with traditional finance failsafes.

This is already happening. RWA TVL crossed $30B last month, up 300% YoY, while DeFi TVL completed a more than 50% drop from the highs. Most RWA TVL is not DeFi yield yet, but the direction is clear.

Capital wants access to real yield, but it also wants real safeguards. Bringing offchain yield onchain is not free. It requires infrastructure that can satisfy both crypto users and institutional allocators. The product has to be transparent enough for DeFi, but robust enough for TradFi.

Here are three things that make thUSD underwriteable:

Transparent Attestations: Onchain proof of reserves are published continuously, and every dollar of backing is verifiable in real time. One of the many benefits of onchain infrastructure is transparency, which far surpasses reactive quarterly letters.

Offchain Yield Generation: thUSD sources yield from real-world markets, not crypto leverage. The first source is the basis between spot and futures gold on the CME, a venue that processes roughly $35B in daily volume and is already trusted by institutional allocators. The second is trade finance: thGOLD lends physical gold to established retailers, like Mustafa Gold, one of Asia’s largest, who use it for inventory and return it with interest.

Institutional Custody: Reserves are managed by Wellington Management, with infrastructure from Standard Chartered’s Libeara. These are the same institutions that custody and administer trillions in traditional markets, now connected to crypto-native infrastructure.

This is what the next generation of stablecoins require. A bridge between crypto rails and the world’s largest yield markets.

thUSD is live today.

Swap & stake at app.theo.xyz.

Original X article by Ari Pingle.