DeFi Isn't Dying, It's Dividing

·

4

MINUTES

·

By:

Ari Pingle

Today, thUSD is live.

The yield-bearing stablecoin powered by the world's deepest commodity market, physical gold, is now available. Genesis Program participants can claim at thusd.theo.xyz. thUSD is also tradeable on Uniswap v4 and stakeable through the Theo app.

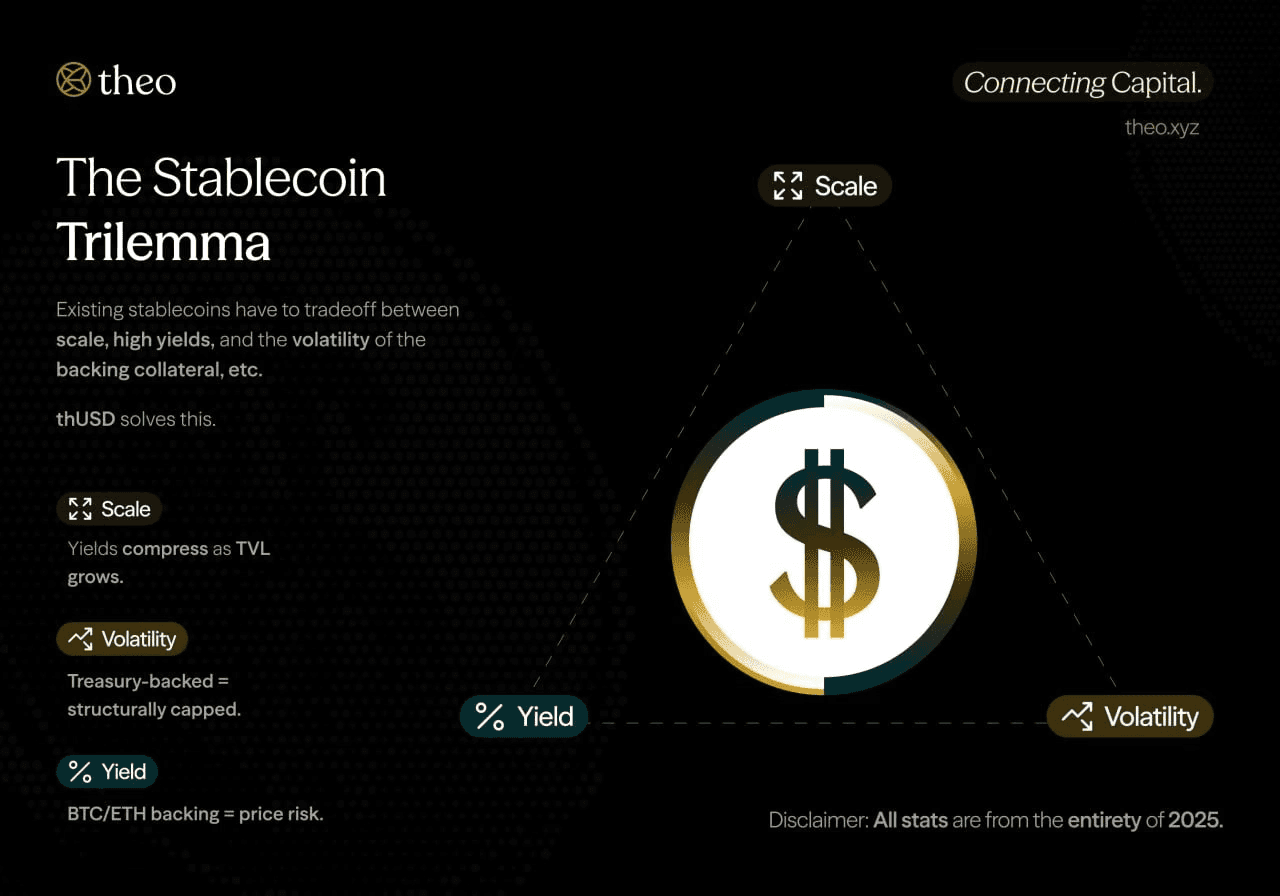

Two months ago, we introduced thUSD as a structural rebuild of the yield-bearing stablecoin. The thesis: every existing design sits inside a trilemma:

Limited capacity

Volatile collateral

Low yield

And the only way out is to anchor yield in a market deeper than crypto by orders of magnitude.

That market is gold. Today, the structure goes live.

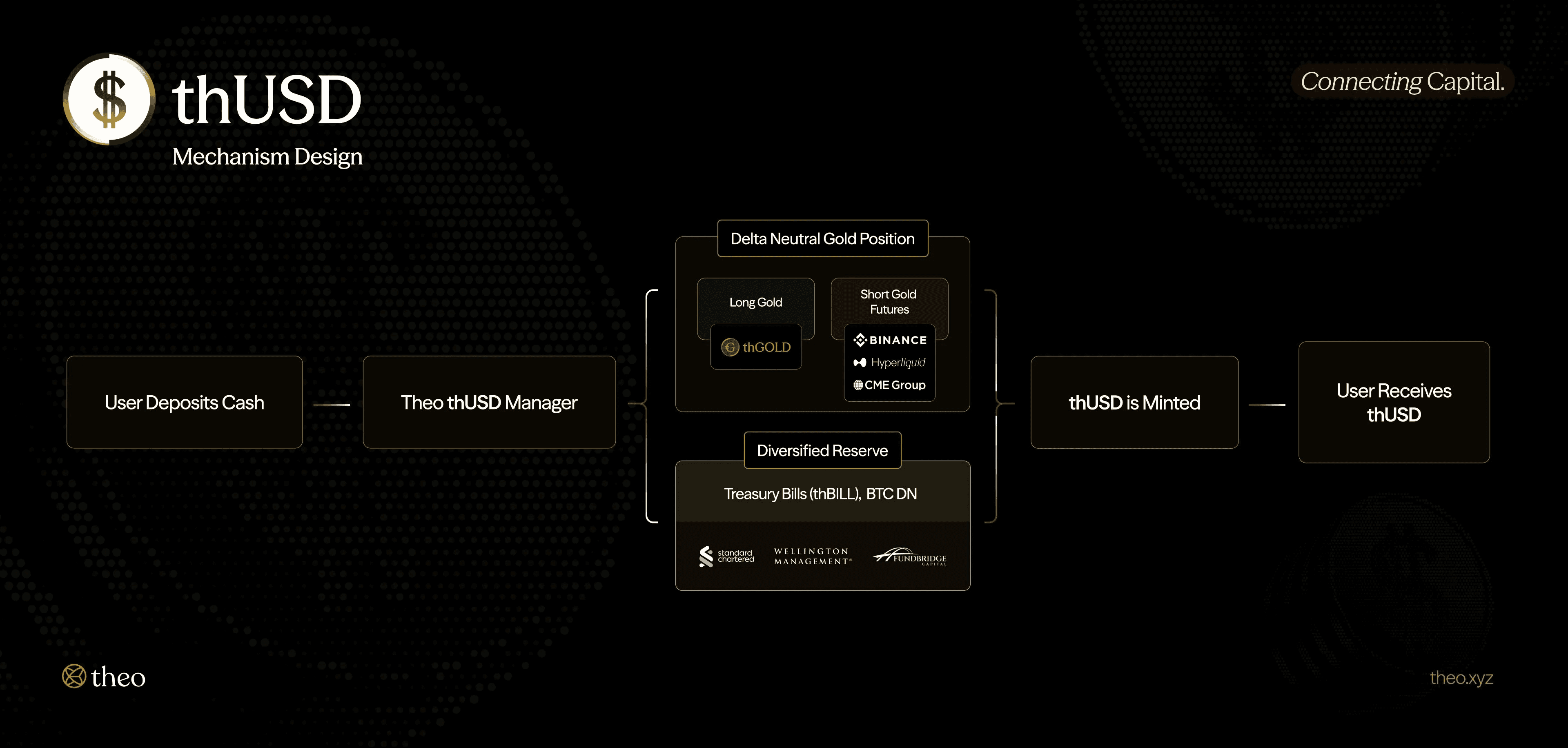

How thUSD Works

thUSD is powered by thGOLD, Theo's tokenized yield-bearing gold product. When thUSD is minted, collateral goes long thGOLD and shorts CME gold futures, creating a delta-neutral position that generates yield regardless of which way spot moves.

The yield comes from two structurally independent sources:

thGOLD lending yield. Gold is lent to established retailers — businesses that need physical inventory for working capital. The fund is operated by FundBridge Capital with security over gold inventory and a 20% first-loss buffer. Tokenization infrastructure runs through Libeara, a Standard Chartered subsidiary.

Gold futures basis and roll yield. thUSD shorts CME gold futures against the long thGOLD position. The spread between physical gold and futures has been a steady source of return for institutional traders for decades. CME is the world's most liquid regulated derivatives venue, which is what lets this carry scale without yield compression.

These two streams are supplemented by a diversified reserve of cash equivalents (including thBILL) and digital assets, providing a layered backing structure.

Why Gold

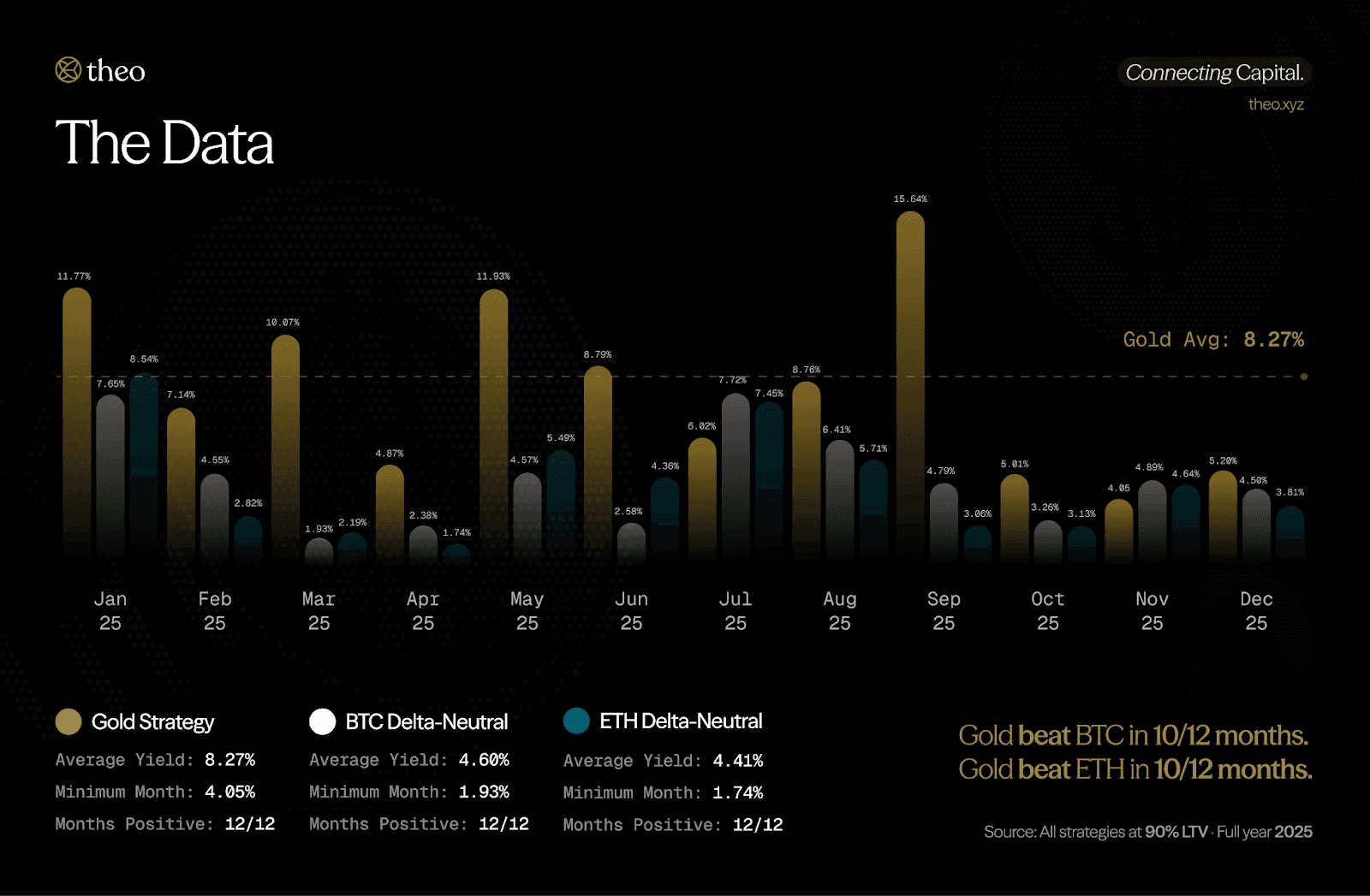

Most yield-bearing stablecoins compress as TVL grows. The math is structural: their yield sources, perp funding, basis trades on BTC and ETH, RWA wrappers on T-bills, are bounded by the depth of the underlying market. Gold isn't.

$247B+ in average open interest on gold derivatives: 39x BTC, 58x ETH

14.4% annualized volatility, compared to 33.5% for BTC and 60.8% for ETH

8.27% average APR on the same delta-neutral structure run on Theo's balance sheet through 2025, with positive yield every month

This is a different scale of market. thUSD can grow to hundreds of billions in TVL while maintaining its yield profile, something no crypto-collateralized alternative can claim.

Read more about thGOLD here.

Security

thUSD launches into an environment where stablecoin failures have cost users billions. The architecture is built for that reality:

Over 95% of collateral sits offchain in physical gold inventory and CME margin, outside the onchain attack surface.

Minting is gated to whitelisted counterparties only.

Transfers cannot route to non-whitelisted parties at the protocol level.

A real-time collateral ratio check enforces a strict floor before any new supply can be issued.

Custody, settlement, and verification flow through FundBridge Capital and Libeara.

Every claim above is verifiable in real time on the transparency dashboard, live from launch.

Full architecture documentation is in the Theo docs.

What's Next

Genesis Program participants can claim today at thusd.theo.xyz and choose to

stake into sthUSD to keep earning, or

claim thUSD directly.

For everyone else, thUSD is tradeable on Uniswap v4 against USDC, with the pool seeded at launch.

Larger gold loan deployments will roll out over the coming weeks, with each origination posted to the transparency dashboard in real time. As deployment scales, the structure builds capacity that crypto-native alternatives can't match: physical gold turns over orders of magnitude beyond crypto, and Theo's piece of that flow is bounded by counterparty appetite, not by onchain liquidity.

This is what connecting the world's capital looks like in practice: a real cash flow from a global commodity market, made composable with onchain rails.

The gold standard is back.

Disclaimer: Yield figures are approximate and based on the strategy run internally throughout 2025 using historical market conditions. Actual returns may vary and are not guaranteed. thUSD involves exposure to counterparty credit risk on gold retailer borrowers, basis and roll risk on gold futures positions, smart contract risk, and operational risk across multiple execution venues. Security over gold inventory and a 20% first-loss buffer mitigate but do not eliminate credit risk. Investors should review the full risk disclosures before depositing. Past performance does not indicate future results.