How thUSD Turns Gold Market Carry Into Dollar-Denominated Yield

·

5

MINUTES

·

By:

Theo

Announcing thUSD Points: our largest points campaign to date.

This blog contains everything you need to know about the thUSD Points Program, including:

How to earn points

How to track points

Our new thUSD Referral Program

We'll also provide details on the previous season of Theo points.

How to Earn Points

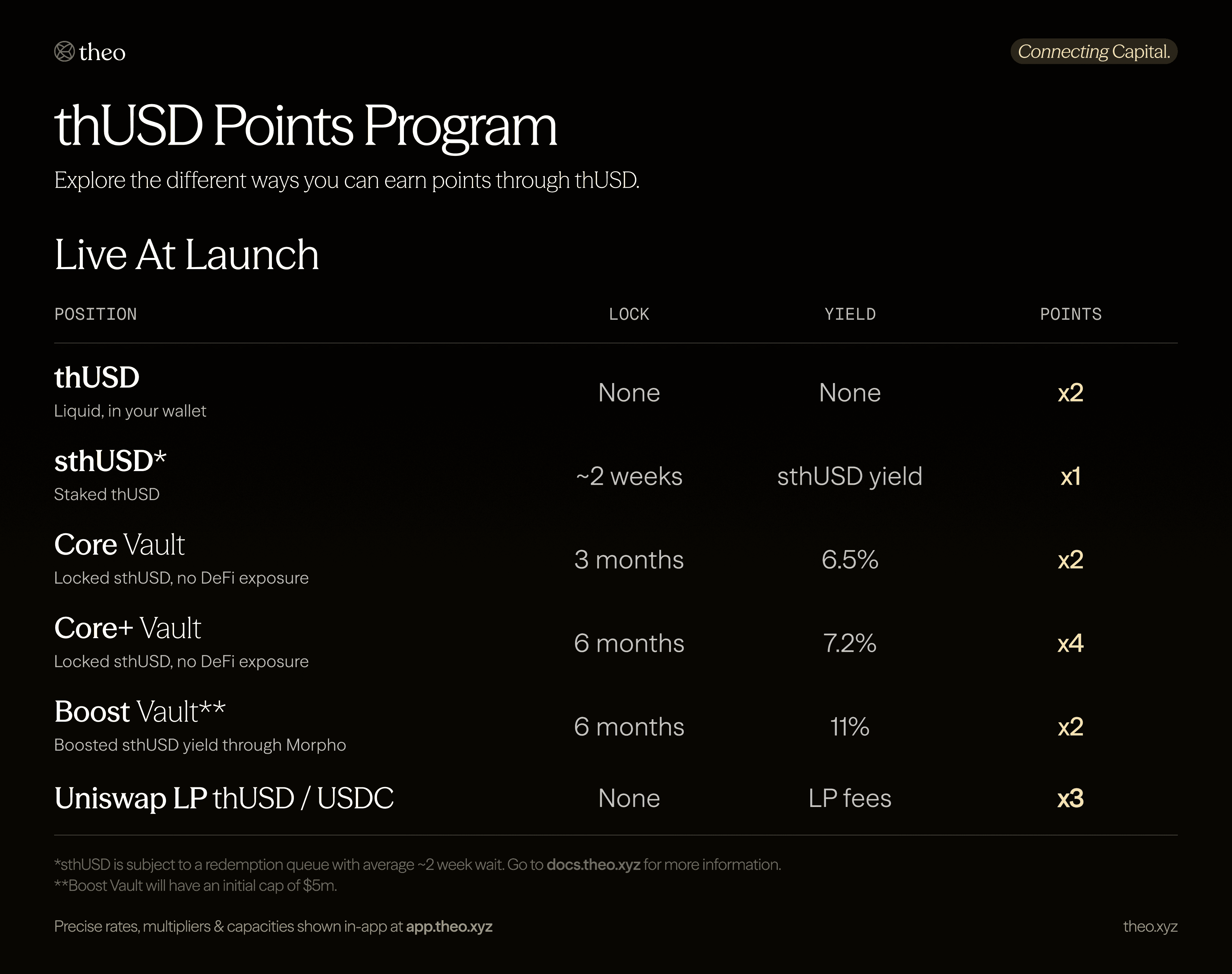

The thUSD Points Program is centered around our flagship product: thUSD.

There are three ways to earn points:

Liquid: hold thUSD or stake your thUSD and receive sthUSD*

Core (and Core+): Locked sthUSD, no DeFi exposure.

Boost: Boosted sthUSD yield through Morpho

*Note: sthUSD is subject to a redemption queue with average ~2 week wait. Go to docs.theo.xyz for more information

Three vaults are live at launch:

3-month Core vault at 6.5% APY

6-month Core+ vault at 7.2% APY

6-month Boost vault at 11% APY, initial cap of $5M

All vaults accept thUSD, USDC, and USDT, and return thUSD, so your position keeps earning yield while it accrues points. Participating in vaults earns the highest native multiplier.

For more info on vaults, thUSD and sthUSD, visit our docs at docs.theo.xyz.

View the vaults and start earning points: app.theo.xyz.

How to Track Points

Track your points anytime in the Theo app. Your balance, multipliers, and referral rewards update in real time. The first update for thUSD goes live the first week of July: until then, the points dashboard will not yet reflect balances.

To view your points, visit app.theo.xyz/rewards.

The thUSD Referral Program

Our new thUSD Referral Program is live today in the Theo app.

Referrers earn a 10% points boost on referred TVL, tiered by volume.

Referees get a 10% points boost on sthUSD via code at deposit.

Rewards begin accruing once referred TVL has been held for 7 days.

View the referral leaderboard and start earning at app.theo.xyz.

A Recap of S1

thBILL point holders will be able to see their final points tally in the first week of July. Points for thBILL accrued until June 19th, the week of the last Pendle market for thBILL.

thUSD Genesis participants can expect to earn a boost to their points. More information on this will be following in the coming weeks.

To view your points, visit app.theo.xyz/rewards.

Start earning points: app.theo.xyz.