Tokenized Real-World Assets: $16 Trillion by 2030

·

4

MINUTES

·

By:

Theo

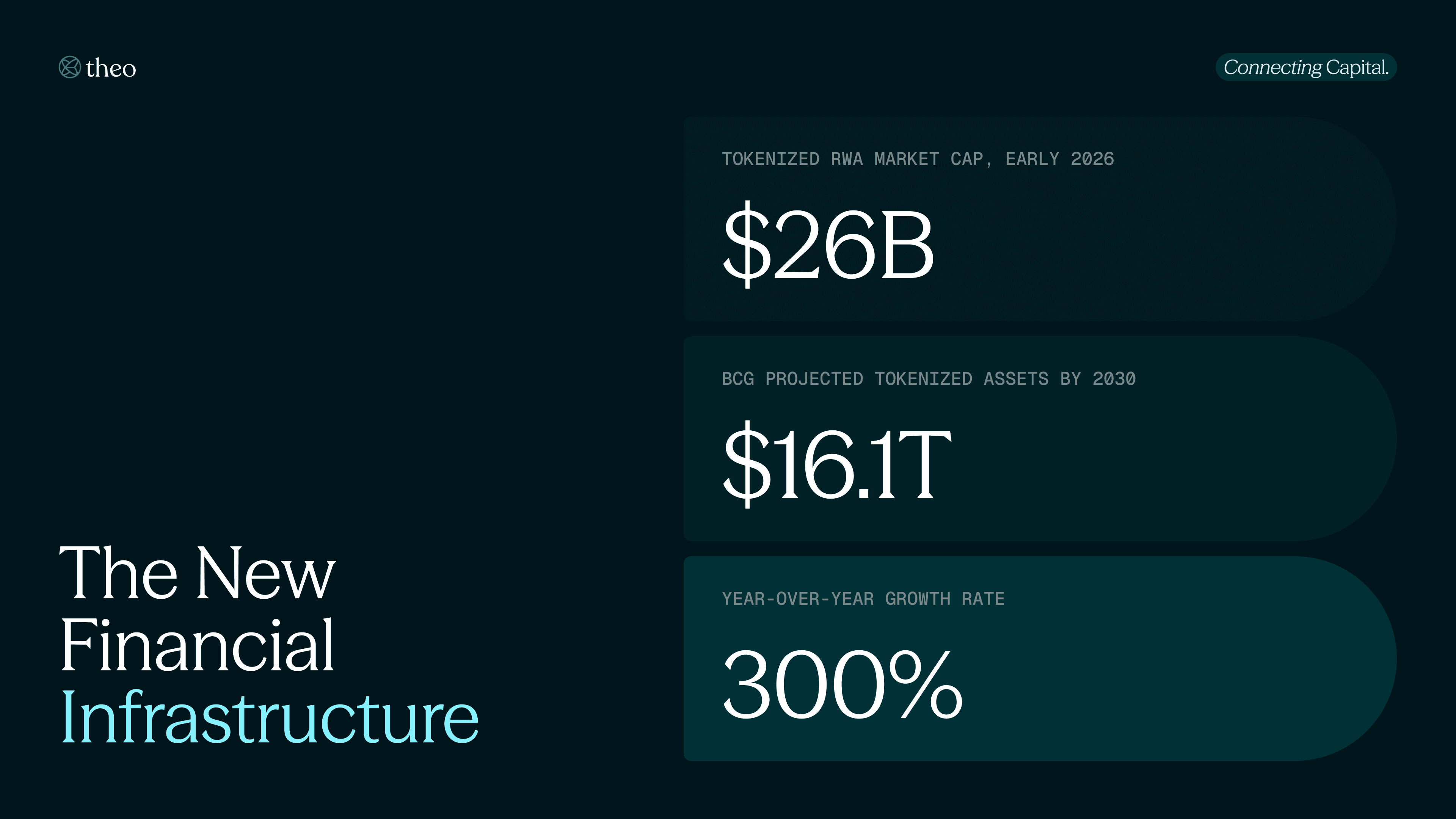

The tokenized real-world asset market crossed $30 billion in early 2026. That figure, representing a 300% year-over-year increase, is drawing attention across institutional desks. It should not. Not because the growth is unimpressive, but because $30 billion measured against what is coming is essentially rounding error.

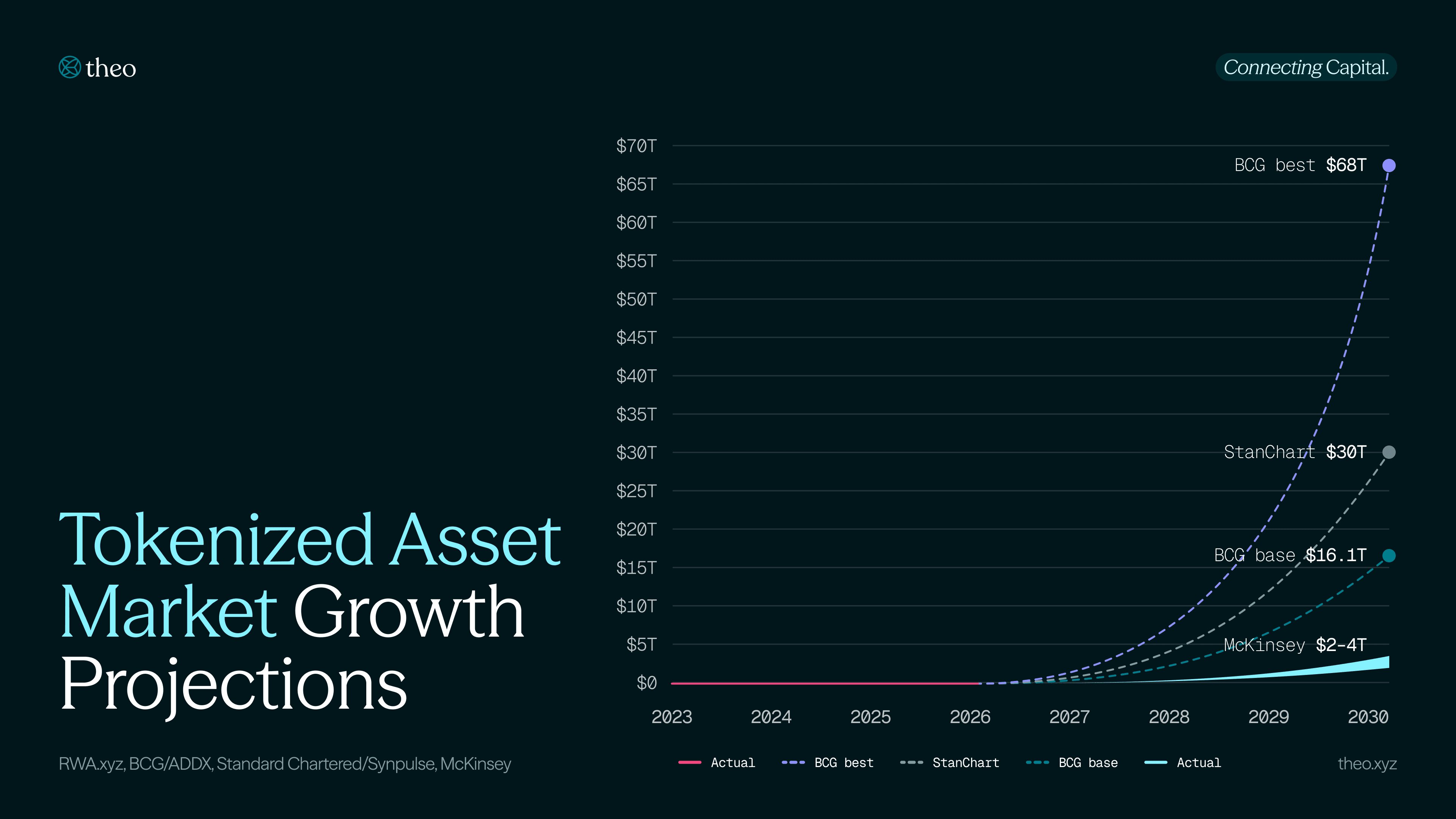

BCG’s projection, published with private markets exchange ADDX, puts tokenized assets at $16.1 trillion by 2030, roughly 10% of global GDP. Standard Chartered goes further: their analysts project $30 trillion in tokenized real-world assets by 2034. McKinsey lands more conservatively at $2 to $4 trillion by decade’s end. Even the floor of these estimates represents a 75x increase from where markets stand today.

The question worth asking is what, precisely, unlocks the curve, and whether the infrastructure being built today is designed to handle the scale that arrives on the other side.

The architecture of $400 trillion in illiquid assets

The underlying opportunity is structural, not speculative. McKinsey estimates that more than $400 trillion in global assets are considered illiquid (real estate, private credit, infrastructure, commodities, private equity), assets that are expensive to transfer, difficult to price in real time, and inaccessible to most market participants outside large institutions. Tokenization does not change what these assets are. It changes how they move.

BCG’s $16 trillion estimate breaks down as roughly $5 trillion in real estate, $4 trillion in fixed income and funds, $3 trillion in private equity, $2 trillion in commodities, and $2 trillion in other classes including intellectual property and infrastructure. This is a systematic repricing of how capital is allocated, settled, and held across every major asset class.

What makes the timeline accelerate now, rather than five years from now, is the convergence of three forces that had previously been missing simultaneously: regulatory clarity at the federal level, institutional infrastructure that meets compliance requirements, and a base layer of liquidity large enough to support secondary market function.

The legislative inflection point

For years, institutional adoption of tokenized assets was constrained not by technology, but by legal uncertainty. That constraint has materially shifted.

The GENIUS Act, the first federal legislation on digital assets to be enacted in the United States, was signed into law on July 18, 2025, after passing the Senate 68 to 30 and the House 308 to 122. The Act establishes a federal regulatory framework for payment stablecoins, requiring 100% reserve backing and clarifying that compliant stablecoins are neither securities nor commodities. For tokenized asset markets, this matters because stablecoins serve as the settlement layer: they are how yield gets distributed, how redemptions are processed, and how capital moves in and out of positions onchain at institutional scale.

The House also passed the Digital Asset Market Clarity Act (known as the CLARITY Act) by a 294 to 134 margin. The bill would clarify which digital assets fall under SEC jurisdiction as securities versus CFTC jurisdiction as commodities, resolving years of enforcement-driven ambiguity that had suppressed institutional engagement.

Together, these two pieces of legislation represent the regulatory scaffolding that institutional participants require before deploying capital at scale. They do not eliminate complexity. They establish the legal perimeter within which compliance teams can operate. That is enough.

Standard Chartered’s head of digital assets research, Geoffrey Kendrick, projects the tokenized RWA market will expand from roughly $35 billion to $2 trillion by the end of 2028, approximately a 56x increase, with stablecoins having “laid the groundwork via increased awareness, liquidity and lending and borrowing onchain for other asset classes, from tokenized money market funds to tokenized equities, to move onchain at scale.”

The institutional floor is already forming

The theoretical demand for tokenized assets has been visible for several years. The structural supply of institutional-grade, onchain products is what lagged. That gap is now closing.

Six individual asset categories now each independently exceed $1 billion in onchain value: private credit, gold and commodities, US Treasuries, corporate bonds, non-US sovereign debt, and institutional alternative funds. BlackRock, Franklin Templeton, and JPMorgan have all moved from pilot programs to live products. The experiment phase is over.

What the market now demands is yield-bearing infrastructure that can scale: products that earn in multiple market conditions, that are transparent in their mechanics, and that can settle in real time across time zones without the friction of traditional custody chains.

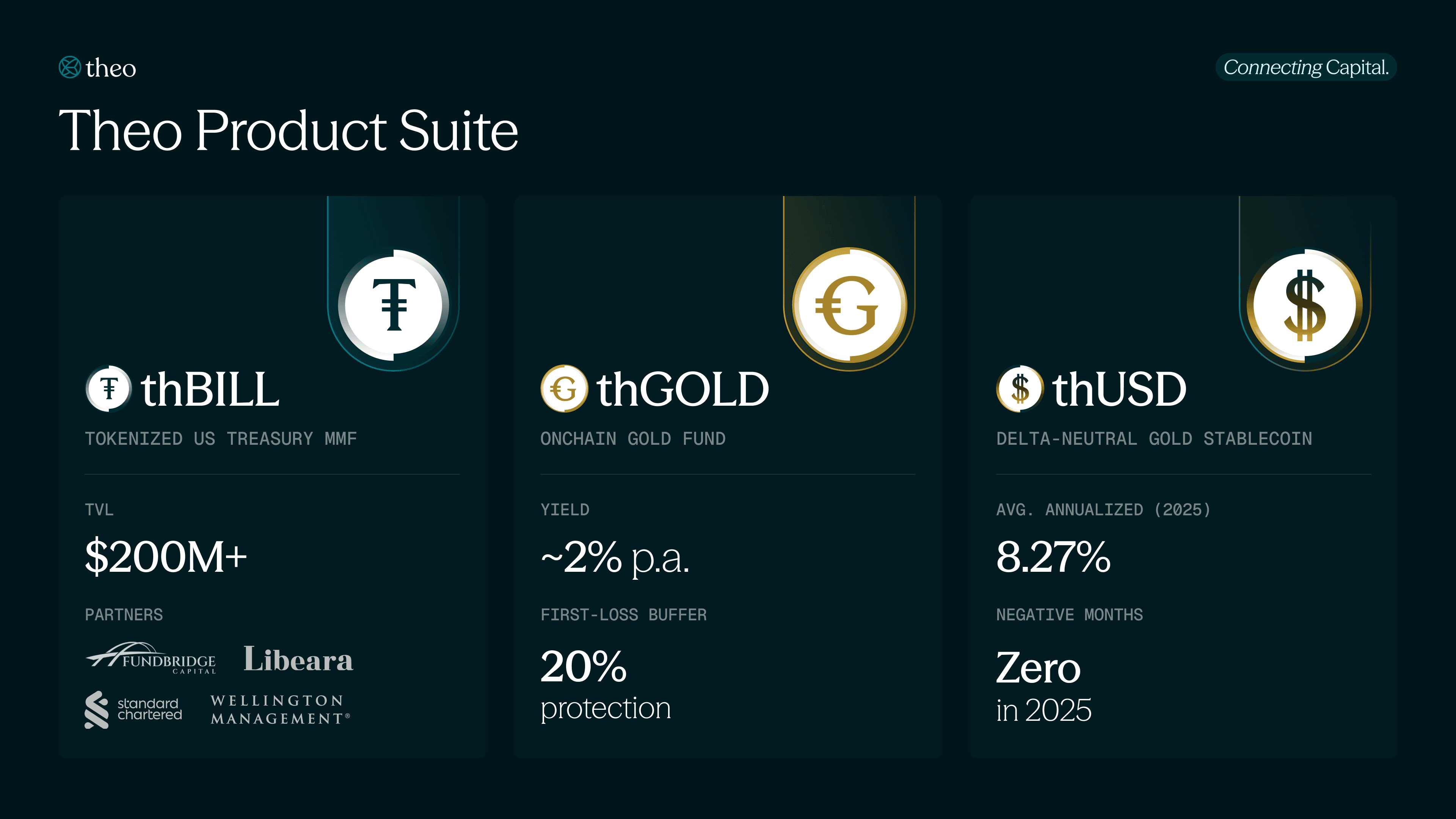

This is where Theo’s product suite is directly relevant. thBILL, built with Standard Chartered’s Libeara platform and Wellington Management, provides tokenized exposure to short-duration US Treasury instruments and currently holds over $200 million in TVL across Ethereum, Base, Arbitrum, and HyperEVM. thGOLD tracks the MG999 Onchain Gold Fund and generates approximately 2% annual yield by lending gold to established retailers, with a 20% first-loss buffer and security over underlying inventory. thUSD, Theo’s gold-backed delta-neutral stablecoin, uses the same gold exposure while simultaneously capturing futures basis on CME, averaging 8.27% annualized over 2025 without a single negative month.

These are asset-class primitives: composable, liquid, and built for the kind of institutional participation that a $16 trillion market requires as its user base.

The shape of the curve

The current $30 billion figure looks large against the baseline of three years ago, when the market was effectively sub-$1 billion excluding stablecoins. It looks small against almost any projection of where it is headed.

BCG’s base case puts asset tokenization at $16.1 trillion by 2030; in a best-case scenario, that estimate reaches $68 trillion. The range is wide because the outcome depends heavily on how quickly the institutional capital stack (pension funds, sovereign wealth vehicles, asset managers) decides to migrate from legacy settlement infrastructure to onchain equivalents. The regulatory conditions for that migration now exist. The market infrastructure is being built in parallel.

The firms that will matter at $16 trillion are the ones building the infrastructure today, when $30 billion still looks like a niche.

Sources: RWA.xyz, BCG/ADDX (2022), Standard Chartered/Synpulse (2024), McKinsey (2023), The Block, Jones Day. All market size figures exclude stablecoins.