Better Rails, Bigger Markets: Why Tokenization Wins

·

6

MINUTES

·

By:

Theo

Over the past two years, it has become clear that public blockchains are not just an alternative venue for digital assets: they are an entirely superior settlement layer for financial markets. They combine continuous market hours, fast global finality, and trustless composability into a single environment.

We believe the next stage of financial market development is the migration of traditional financial assets onto these rails in the form of Real-World Assets (RWAs).

While there are designs to create synthetic RWAs, we outline below the case for tokenization as a far superior alternative. Its value is not in purely digitizing traditional financial assets, but in enabling them to interact natively with the capital-efficient, integrated market structure that already exists onchain.

Our thesis is straightforward:

Blockchains are superior rails for financial markets.

The time is here to bring traditional financial assets onchain.

Tokenization is the superior mechanism to do so.

Better Rails for Finance

The operational superiority of onchain markets has been long evident in crypto-native products.

They operate continuously and globally without market hours, settle transactions with finality in seconds rather than days, and allow collateral to be moved and reused across venues without friction.

Price discovery, execution, and settlement all occur within the same permissionless environment, reducing reliance on centralized intermediaries.

Until now, the core downside of crypto-native products has been the User Experience (UX). However, with considerable progress having been made at the wallet, chain, and indexing layers, the experience of interacting with modern crypto protocol is akin to that of Web2 applications.

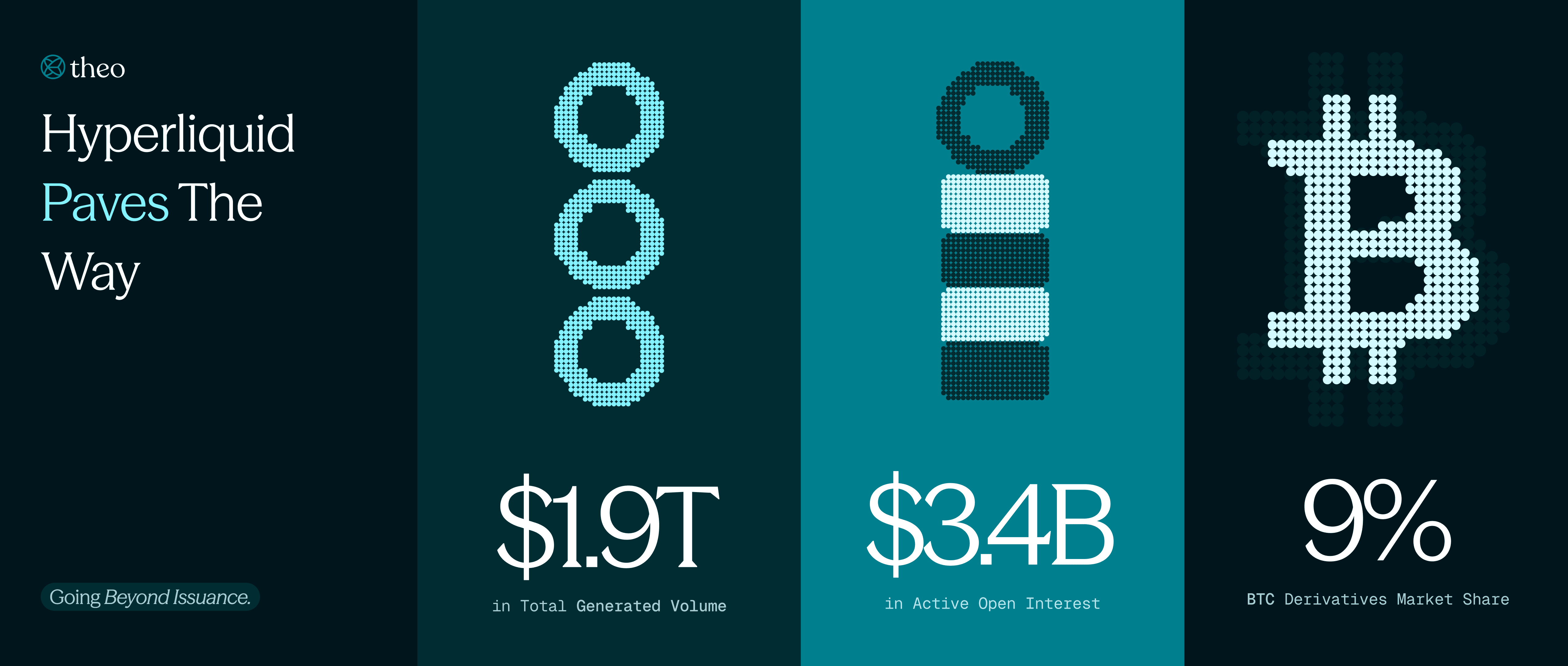

Hyperliquid Paves the Way

Over the past year, the explosion of perpetual futures has acted as a direct test of whether onchain infrastructure can sustain the demands of high-volume, continuous trading.

Specifically, Hyperliquid has tested the limits of onchain infrastructure with resounding success.

Hyperliquid has processed over $1.9 trillion in volume over the past 12 months, including $300+ billion in July alone.

Today, it has over $3.4 billion in open interest on Bitcoin contracts, corresponding to nearly 9% of the Bitcoin derivatives market.

All the while, Hyperliquid has maintained an exceptional user experience, with spreads on Bitcoin as low as just one Dollar. This demonstrates that public blockchain infrastructure can handle sustained institutional-scale throughput, without sacrificing on its core promise of permissionlessness, or executional quality.

The ability of public blockchains to support large-scale finance eliminates a key barrier in bringing traditional asset classes onto the same rails.

Tokenization Momentum

Tokenization is the necessary process connecting traditional asset classes to onchain rails.

In the first half of 2025, nearly $10 billion of real-world assets were issued onchain by major asset managers and custodians — including notable names like BlackRock and Franklin Templeton.

These first signs of institutional traction demonstrate the feasibility of bringing traditional financial instruments onchain, if just by proving legal and regulatory requirements can be satisfied.

By placing assets like U.S. Treasuries, equities, commodities, and private credit instruments onchain, issuers are positioning these assets (and ultimately their holders) to benefit from the same operational advantages already available to crypto-native instruments:

Low-friction 24/7 trading

Composability with derivatives

Instant collateral mobility

Why Use the Real Thing?

At first glance, a simpler mechanism to create onchain trading venues for RWAs is to create virtual representations of those assets in the form of synthetics or perpetuals contracts.

The former, synthetic assets, suffers from the classic conundrum of not being able to “settle” positions as prices drift. Existing models for synthetics rely on over-collateralized mint-and-redeem systems, which are inherently limited. They are:

Highly capital inefficient

Ineffective for volatile or trending assets

Reliant on oracles

While perpetuals futures contracts have established their legitimacy in the industry, they are only truly effective for assets with spot markets available on crypto-native, on- and offchain venues, such as Bitcoin, Ethereum, or other crypto-native assets.

Why Perps Alone Don’t Work

Our research shows that the assets with the highest perpetuals trading volumes are inherently long-biased. As a result, maintaining a balanced perps market requires the participation of market makers who contribute to short-side liquidity through cash-and-carry — or **just carry for short — trades.

A carry trade entails holding the underlying spot asset while shorting a corresponding perpetuals contract, allowing the market maker to earn the market’s funding rate while remaining delta-neutral.

Executing a carry trade for an RWA is complex, as positions must be rebalanced across two entirely separate environments: onchain and the traditional brokerage. Not only do today’s crypto-native market makers lack the infrastructure to effectively execute this type of trade on traditional venues, but there is also an inherent delay in moving funds between these environments at size.

Together, these factors make perpetuals contracts alone an ineffective mechanism for representing traditional financial assets onchain.

Enter Theo

By starting with tokenization, we’re able to create attractive spot markets that can in turn be used to drive liquidity for derivatives (including perps!) markets. For every Dollar of an asset tokenized, several more Dollars of derivatives can be traded onchain in a liquid and robust way.

For this to hold in practice, however, tokenization must go beyond issuance. Without liquid venues, accepted collateral frameworks, and open-ended composability, an RWA remains economically inert for both traders and market makers.

Integration into the existing onchain market structure is what unlocks capital efficiency gains. At Theo, we achieve this by bootstrapping the integrations and liquidity needed to develop a complete market ecosystem first-hand.

Our tokenized treasury fund, thBILL, demonstrates this in action. thBILL can be traded, posted as collateral, and moved across onchain venues without conversion. It is live today on Ethereum, Base, Arbitrum, and HyperEVM with liquid trading and lending venues across all supported chains. thBILL’s intentional design reflects the demands of active market participants, not just custodial considerations.

By building issuance, mobility, and liquidity into a single system, Theo’s infrastructure makes RWAs functionally equivalent to native onchain instruments.

Outlook

The thesis is already visible in crypto-native markets: the rails are better, and the economic benefits of using them are material. The institutional side is now in the early stages of migration.

The determining factor in adoption speed will be whether RWAs are issued into environments where they can immediately access the same capital-efficient, integrated structure that has made onchain markets competitive. That is the infrastructure gap Theo is addressing.